What is a three-way reconciliation?

Everyone who has balanced a checkbook knows how to perform a two-way reconciliation – you verify that the balance shown on your bank statement, when adjusted for uncleared deposits and withdrawals, matches the balance shown in your books or checkbook.[1]

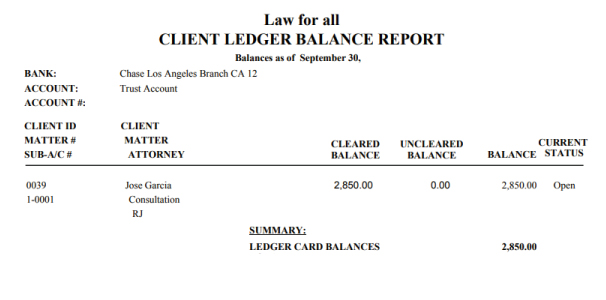

Once you have performed a two-way the reconciliation on the trust account, however, you have to perform a third reconciliation where you check the [simple_tooltip content=’The Client Trust Ledger shows trust fund activity for each matter. The report provides a trust balance for each trust account within the matter as well as matter and client totals.’]client trust ledger[/simple_tooltip] balance against both the adjusted bank balance and the book balance to ensure that all three match.[2] If the trust account is a pooled account such as an IOLTA, then you will have multiple client trust ledgers as well as a ledger for bank charges. The total of all of the ledger balances should match the IOLTA’s adjusted bank balance and book balance.

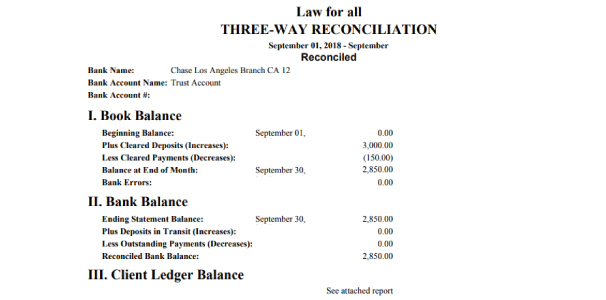

A three-way reconciliation report contains the adjusted bank balance, the book balance, and the client trust ledger balance and shows that all three balances match. The following is a sample of a three-way reconciliation report:

References

1. Attorney Trust 3-Way Account Reconciliation Rules & Your Practice

2. How to Perform a Three-Way Trust Reconciliation